Welcome to another post on reproducibility in finance literature!

A couple of days back, Robeco quant researcher Matthias Hanauer tweeted his latest work (joint with David Blitz) on size premium in the “Settling the Size Matter"1 paper. It’s a relatively short paper and attempts to address the basic question if (and how) size factor matters at all.

Does Size Matter? Check out our brand new paper on the size premium (joint work with David Blitz).

It was a quick fun exercise reproducing the results using Python 🐍. All the code is available on Github

settling-the-size-matter

Data

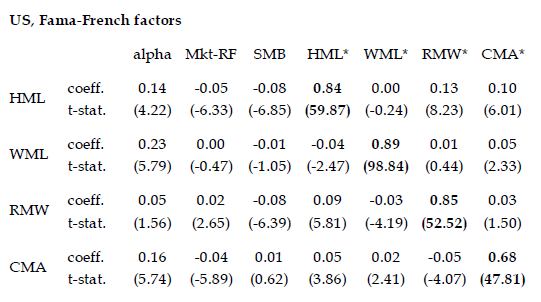

Almost all the data used in the paper is publicly available from following sources (except for their self-constructed size factor based on 2x3 independent sorts on size and the ex ante beta of a stock towards the QMJ factor (SMB_beta_QMJ))

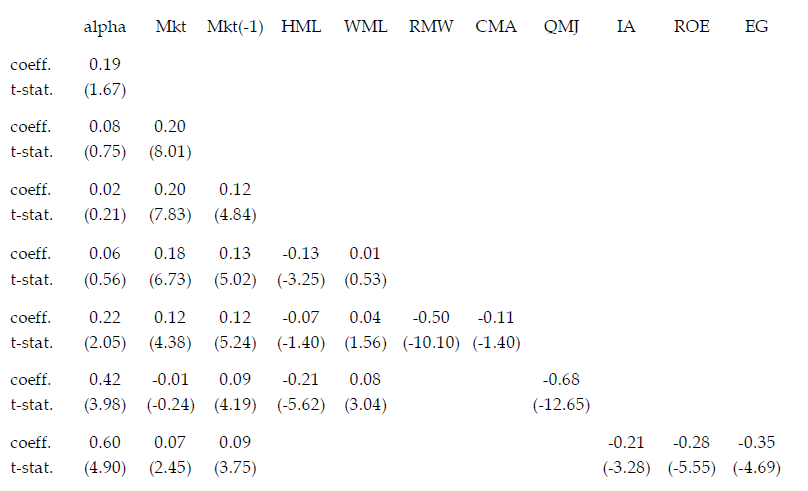

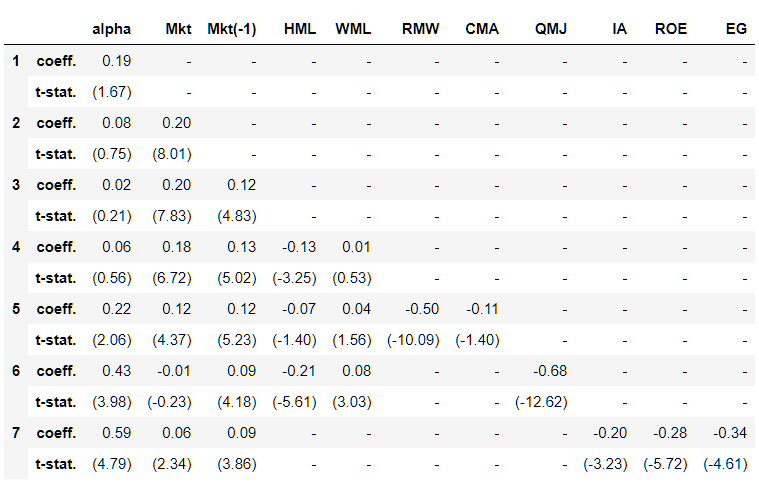

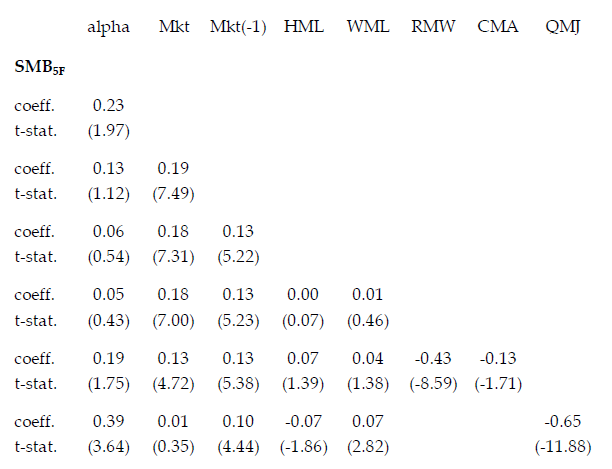

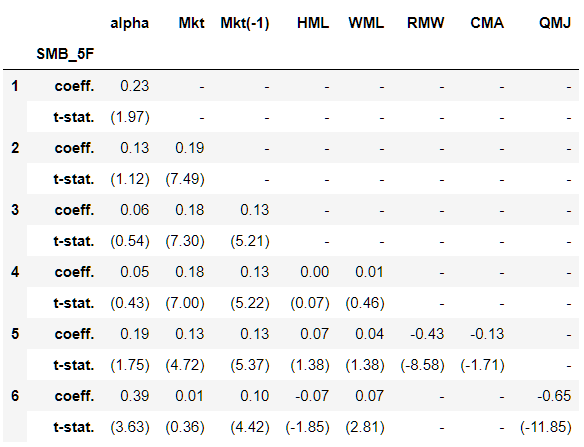

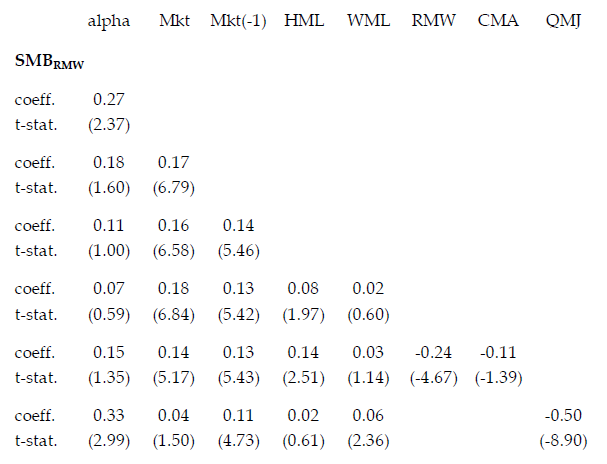

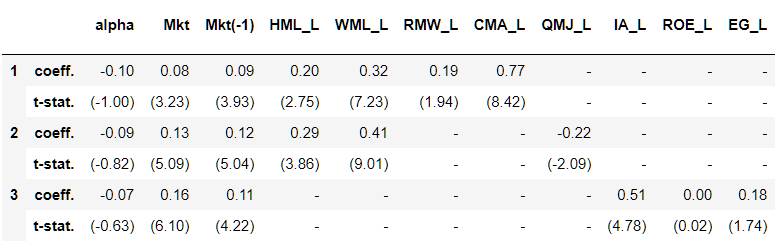

Exhibit 1: Regression results for US SMB_3F factor

There exists a “raw size” premium of 0.19% per month in the US but fades away after controlling for market exposure as well as popular factors of value (HML) and momentum (WML)

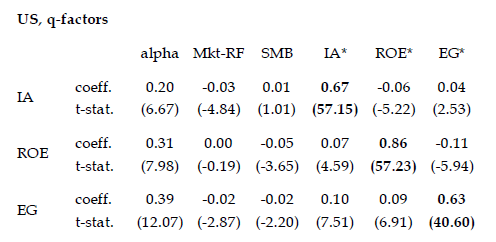

Size premium rises significantly after considering additional factors exposures such as Fama-French’s profitability (RMW) and investment (CMA), AQR’s quality-minus-junk (QMJ) and extended q-factors of investment-to-asset (IA), return on equity (ROE) and expected growth (EG) respectively

Original Paper Table

Reproduced Table

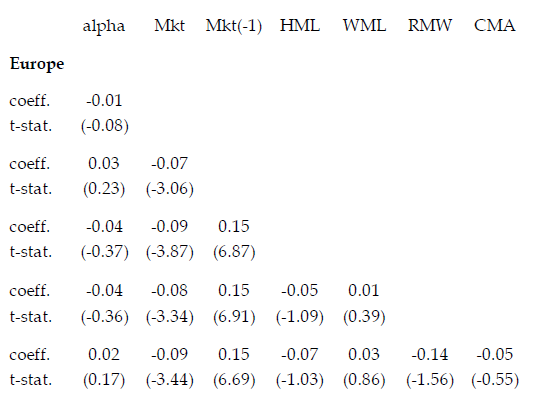

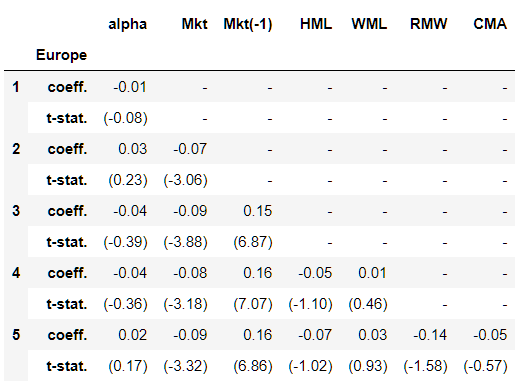

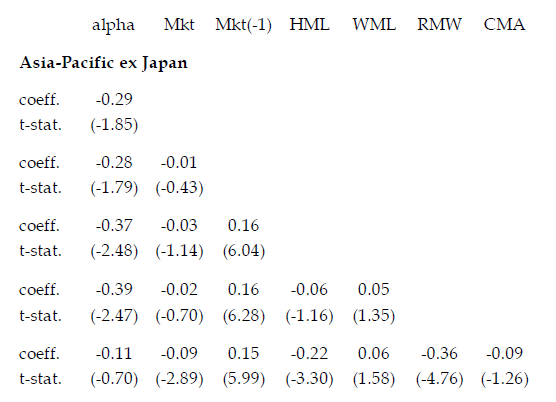

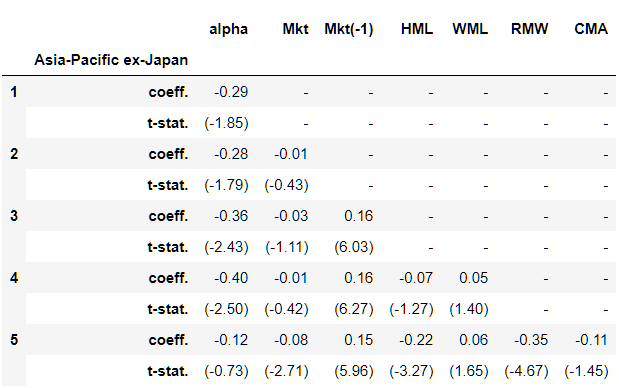

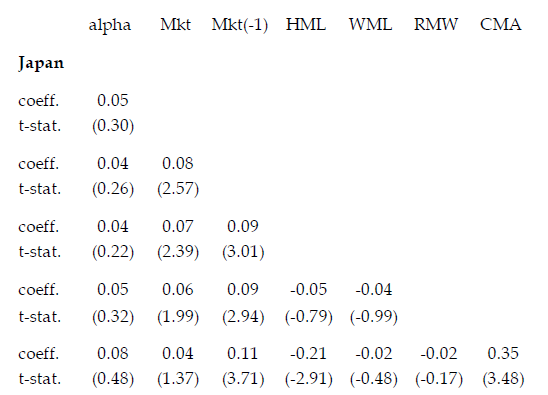

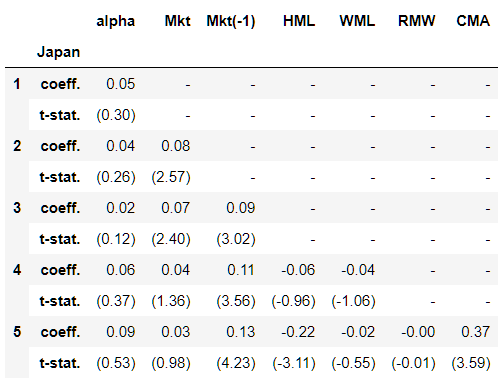

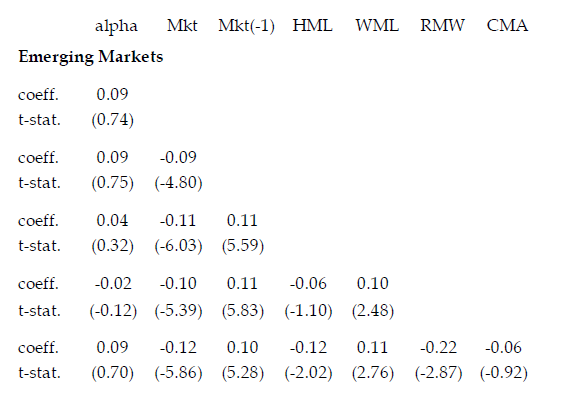

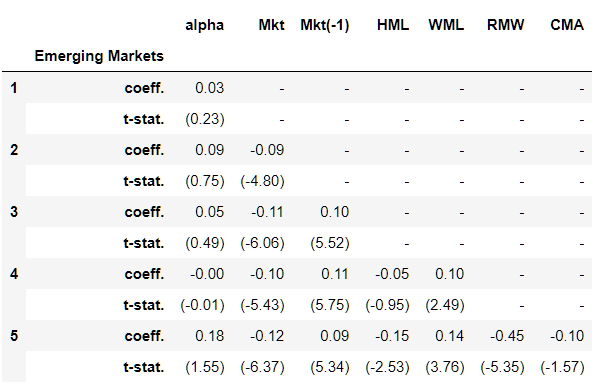

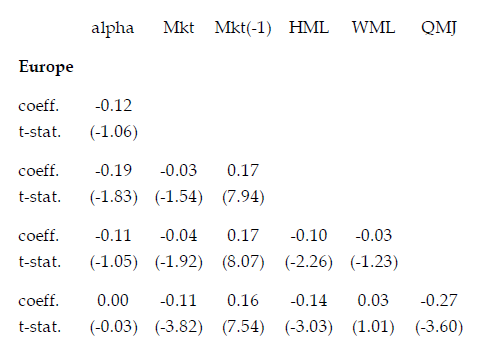

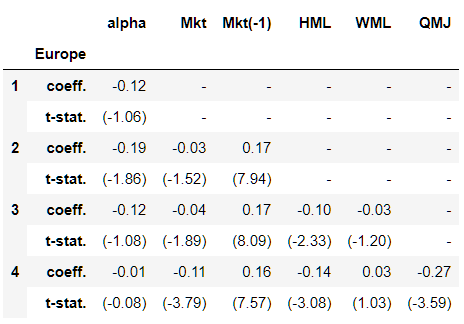

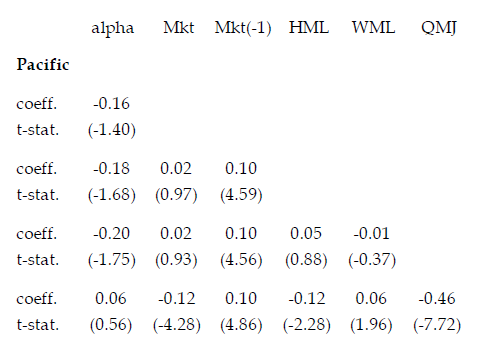

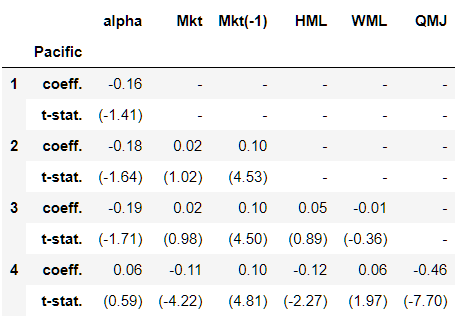

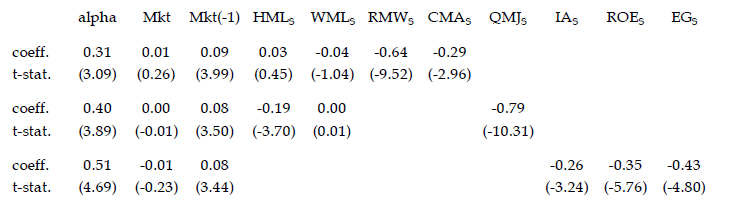

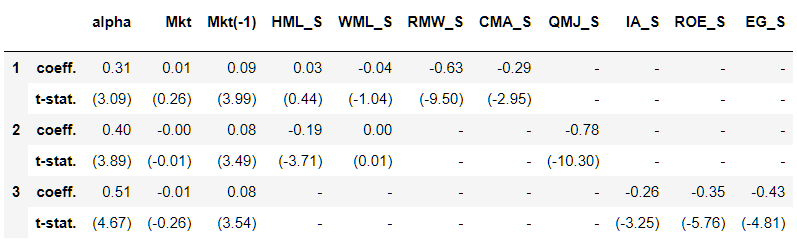

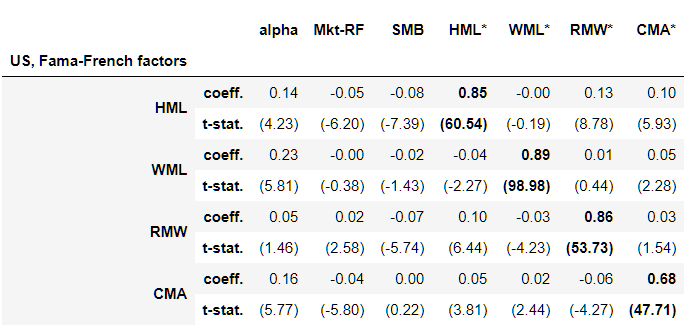

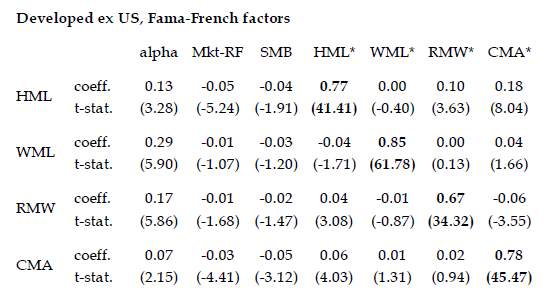

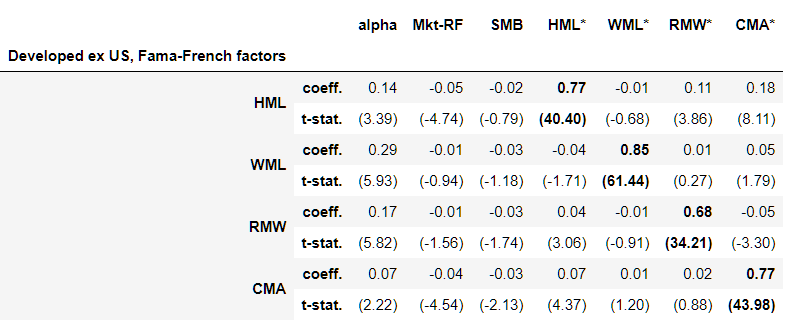

Exhibit 2: Regression results for international SMB_3F factors, Kenneth French regional data

Internationally, the size premium remains absent – discretely as well as when considered with other factor exposures such as HML, WML, RMW and CMA

Europe

Original Paper Table

Reproduced Table

Asia Pacific ex-Japan

Original Paper Table

Reproduced Table

Japan

Original Paper Table

Reproduced Table

Emerging Markets

Original Paper Table

Reproduced Table

Exhibit 3: Regression results for international SMB_3F factors, AQR regional data

Results are similar to Exhibit 2 (i.e. no existence of significant alpha), although it slightly improves after controlling for QMJ factor

Europe

Original Paper Table

Reproduced Table

Pacific

Original Paper Table

Reproduced Table

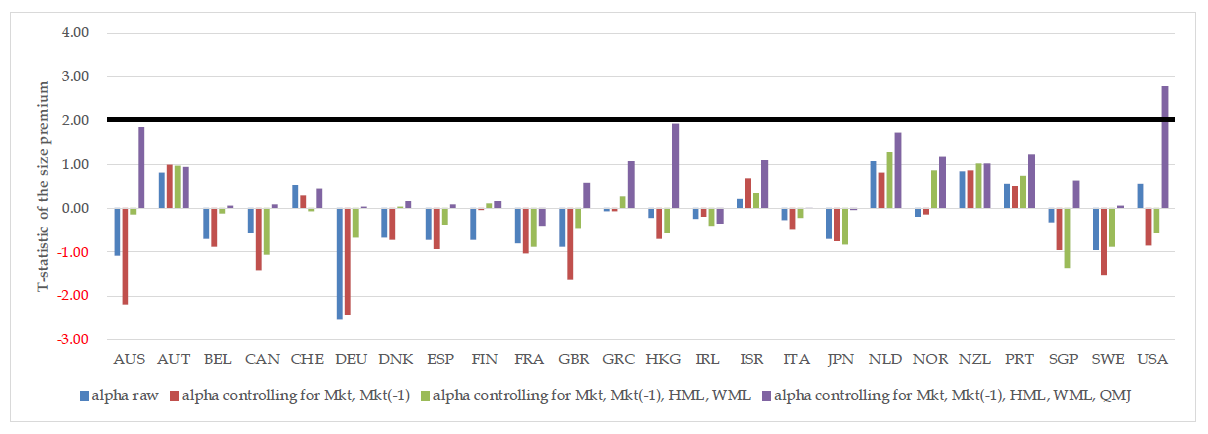

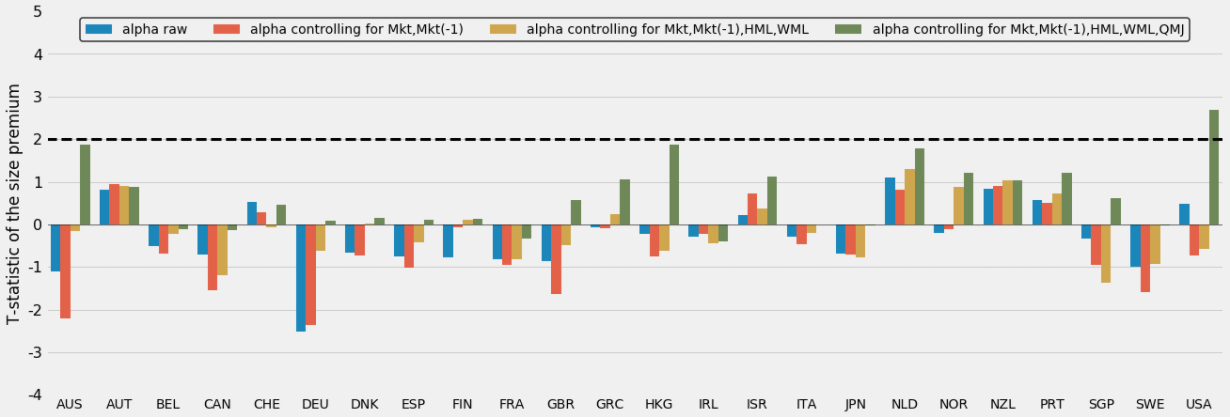

Exhibit 4: Regression results for international SMB_3F factors, AQR country data

For most international markets, the size premium is statistically insignificant with the sole exception of the US (but only after controlling for QMJ factor exposure)

Original Paper Figure

Reproduced Figure

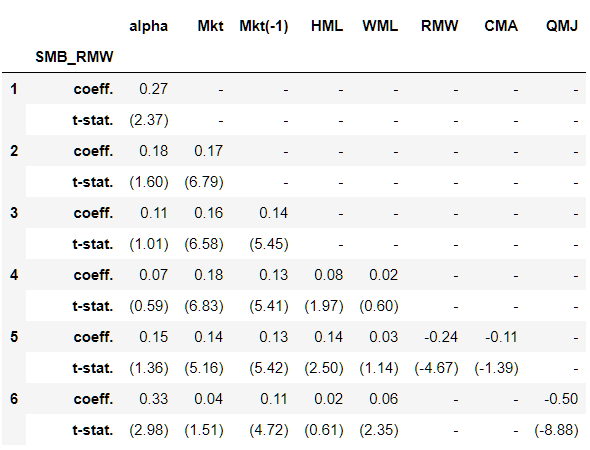

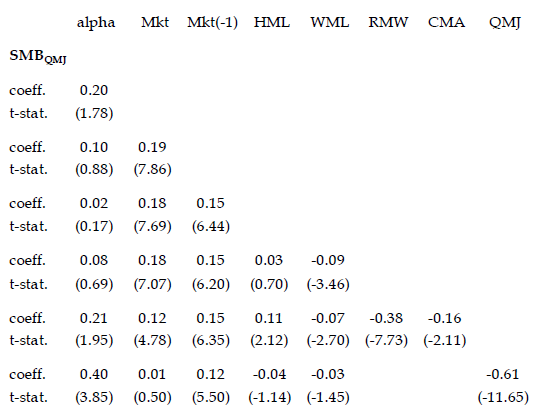

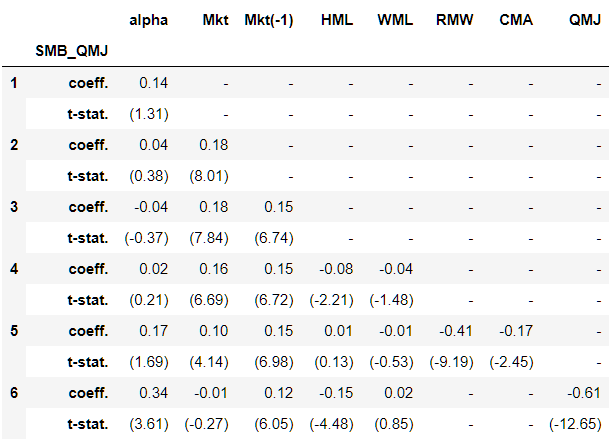

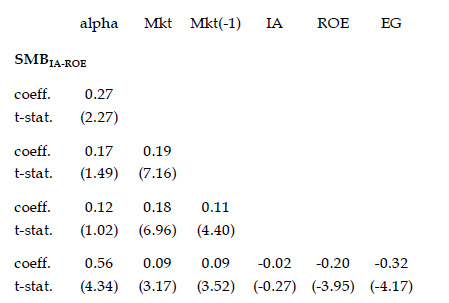

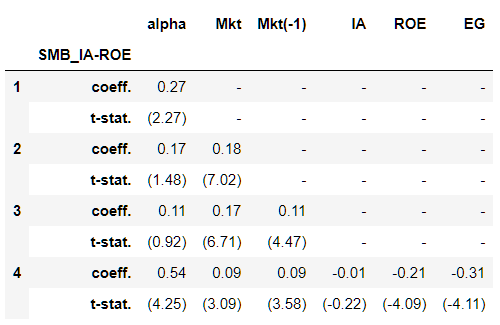

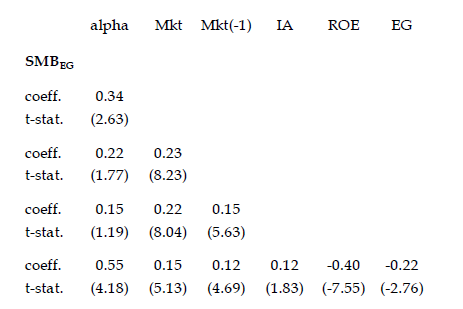

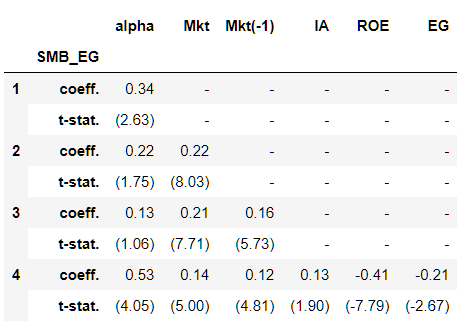

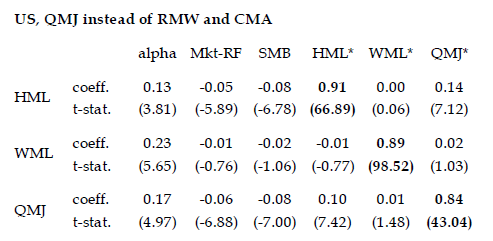

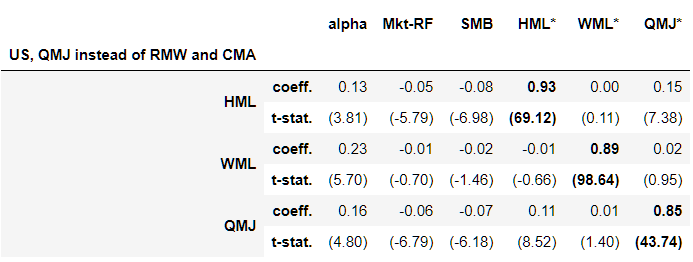

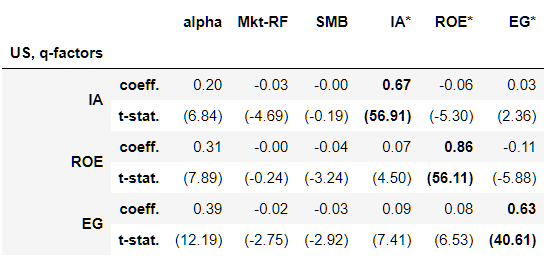

Exhibit 5: Regression results for different versions of the US SMB factor

Considering different versions of quality-controlled ex-ante size factors (as opposed to ex-post in the earlier case) doesn’t alter the results to a significant extent

Original Paper Table

Reproduced Table

Original Paper Table

Reproduced Table

Original Paper Table

Reproduced Table

Original Paper Table

Reproduced Table

Original Paper Table

Reproduced Table

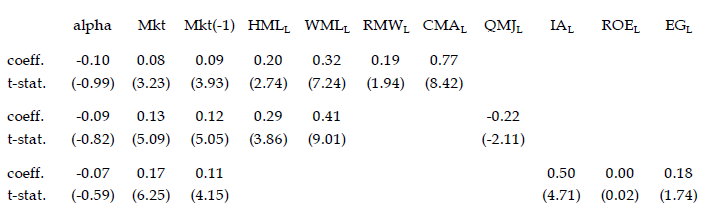

Exhibit 6: Regression results for US SMB_3F on either the long legs or the short legs of other factors

The size premium results are promising but limited only to short leg of other factors

Original Paper Table

Reproduced Table

Original Paper Table

Reproduced Table

Exhibit 7: Regression results for standard factors on alternative factors with 10% instead of 50% weight to small-caps

Size factor plays a key role to fully expose the benefits of other factors such as value and momentum

Original Paper Table

Reproduced Table

Original Paper Table

Reproduced Table

Original Paper Table

Reproduced Table

Original Paper Table

Reproduced Table

Summary

The key message of the paper is quoted from the last line of the abstract

“Size is weak as a stand-alone factor but a powerful catalyst for other factors”